Eurozone Inflation Undershoot, China Tech Controls and USMCA Jolt Redraw Risk Map

Severity: WARNING

Detected: 2026-07-01T09:20:29.828Z

Summary

In the 08:00–09:00 UTC window, core pillars of the global macro and trade architecture shifted at once: Eurozone inflation eased faster than expected, Beijing locked down outbound tech investment under national security rules, and Washington signaled it may not renew USMCA. Combined with fresh sanctions on Iran-linked crypto flows, a major new Ukraine aid package and an emerging funding cliff for UNRWA, the risk picture for rates, tech supply chains, North American manufacturing and Middle East stability is materially changing in real time.

Details

Between 08:00 and 09:00 UTC, a cluster of developments re-shaped key macro, trade and geopolitical risk lines that senior leadership and trading desks will need to reprice quickly.

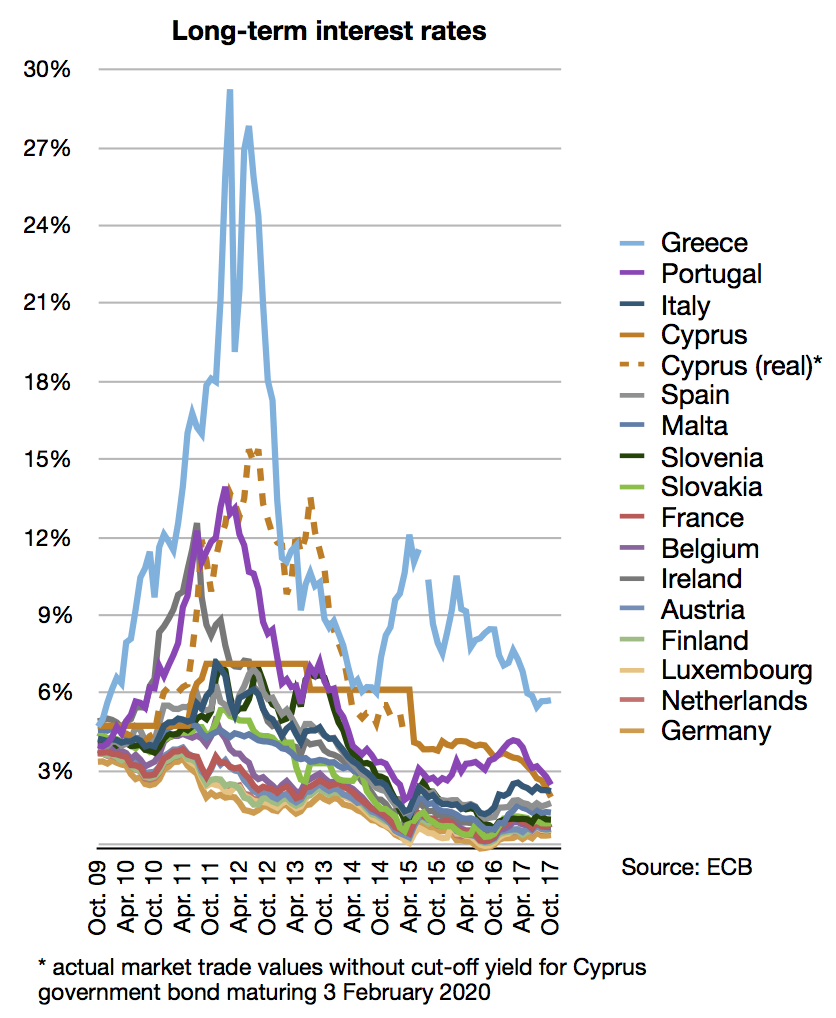

At 09:00 UTC, flash data showed Eurozone June CPI rising 2.8% year-on-year, below the 3.0% market forecast. This is a meaningful downside surprise to expectations of sticky inflation. For the European Central Bank, it strengthens the case for additional cuts in 2H 2026 and will pull forward rate-cut pricing. Sovereign yields in the periphery and core are likely to compress, supporting duration and rate-sensitive equities while marginally weakening the euro against the dollar. For households and corporates, a more dovish ECB path would ease financing costs but also signal softer demand conditions in key industrial economies like Germany and Italy.

At 08:22 UTC, Beijing published official regulations imposing national security rules on overseas investments and offshore tech transfers. This is a structural move, not rhetoric. It codifies state security primacy over commercial logic in Chinese outbound capital and technology deals, reinforcing the decoupling trend in semiconductors, AI, telecoms and critical infrastructure. Multinationals relying on Chinese investment or JV technology flows in Europe, Southeast Asia, Africa and Latin America now face higher approval risk, slower deal timelines and elevated political interference. Global tech valuations, especially in hardware and supply-chain names, will need to discount higher friction and the prospect of parallel technology spheres.

At 08:16 UTC, reports indicated Washington is expected not to agree to extend USMCA for another 16-year term at the mandatory six-year review. While this does not terminate the pact immediately, it injects uncertainty into the medium-term rules governing roughly US$1.5 trillion in annual North American trade. Automakers, agriculture, energy pipelines and cross-border manufacturing – especially in Mexico-based assembly hubs – are most exposed. Currencies (CAD, MXN) and regional industrials will likely price in higher long-term political risk premia and potential renegotiation shocks.

In the security space, Israel at 08:30 UTC announced sanctions on dozens of cryptocurrency wallets linked to Iran’s IRGC, explicitly aiming to choke off terrorist financing routes. This signals a more aggressive, technically sophisticated enforcement posture and raises compliance risk for crypto exchanges, DeFi protocols and OTC brokers with any Iran-adjacent flows. It further tightens financial pressure on Tehran at a moment when Iranian officials (09:00 UTC) are issuing renewed, time-bounded threats of ‘revenge’ operations abroad, sustaining elevated regional security risk around Israel, Gulf shipping and Western targets.

At 08:25 UTC, UN Secretary-General António Guterres warned that UNRWA – the lifeline for millions of Palestinian refugees – could collapse due to a severe funding shortfall. A financial failure of UNRWA would sharply worsen humanitarian conditions in Gaza, the West Bank, Jordan, Lebanon and Syria, raising the odds of social unrest, cross-border displacement and pressure on neighboring governments already under fiscal and political stress. For markets, this raises tail risks of renewed spikes in Middle East instability, which historically correlate with higher oil and gold prices.

Denmark at 08:52 UTC announced a new military aid package for Ukraine worth 4.4 billion Danish kroner (about €590 million), including weapons, ammunition, equipment and training funds. This is a significant top-up from a mid-sized NATO member and a clear signal that European support is not degrading. It sustains Ukraine’s capacity to absorb Russian pressure and conduct limited offensives, and locks in continued demand for European and US defense production, supporting defense contractors and munitions suppliers.

Separately, Venezuela is coping with a major earthquake in La Guaira, with new viral footage at 09:00 UTC showing the collapse of four residential buildings, up from two previously seen in earlier recordings. While the quake is primarily a humanitarian emergency, it adds stress to an already fragile state and may disrupt local logistics, coastal infrastructure and insurance exposure in a Caribbean-adjacent corridor used by some shipping lanes.

In Russia and Ukraine, reports of a substation failure in Moscow region under concurrent UAV attack (08:09 UTC) and continued Ukrainian strikes on Russian energy and industrial targets fit the existing pattern of mutual infrastructure pressure rather than a clear new escalation threshold.

In the next 24–48 hours, watch for: ECB officials signaling how the CPI miss affects their September and December meetings; detailed Chinese regulatory text clarifying the scope of ‘national security’ in outbound tech deals; formal US language on USMCA review outcomes and any reaction from Ottawa and Mexico City; secondary sanctions or enforcement actions following Israel’s IRGC crypto move; donor reactions to Guterres’s UNRWA warning – especially from the US, EU and Gulf states; and initial loss, infrastructure and port-impact assessments from the La Guaira earthquake. Trading desks should reassess exposure to European rates and FX, North American auto and manufacturing supply chains, global tech hardware names linked to Chinese capital, and Middle East risk proxies including oil, gold and regional FX.

MARKET IMPACT ASSESSMENT: Eurozone CPI miss supports earlier ECB easing, likely pressuring euro and supporting regional equities and bonds; China’s outbound-investment security rules raise risk premia on Chinese tech, outbound M&A and global supply chains; IRGC crypto-wallet sanctions signal tighter enforcement on Iran-linked finance, marginally adding to Gulf risk premia; potential UNRWA collapse and Gaza/Palestinian instability could feed Mideast headline risk; prospective non-renewal of USMCA would be a medium-term bearish overhang for CAD/MXN-sensitive supply chains and autos; Venezuela quake adds immediate local infrastructure and insurance risk, with possible sentiment spillovers to EM credit; continued robust Ukraine aid reinforces European defense and energy-complex trades.

Sources

- OSINT