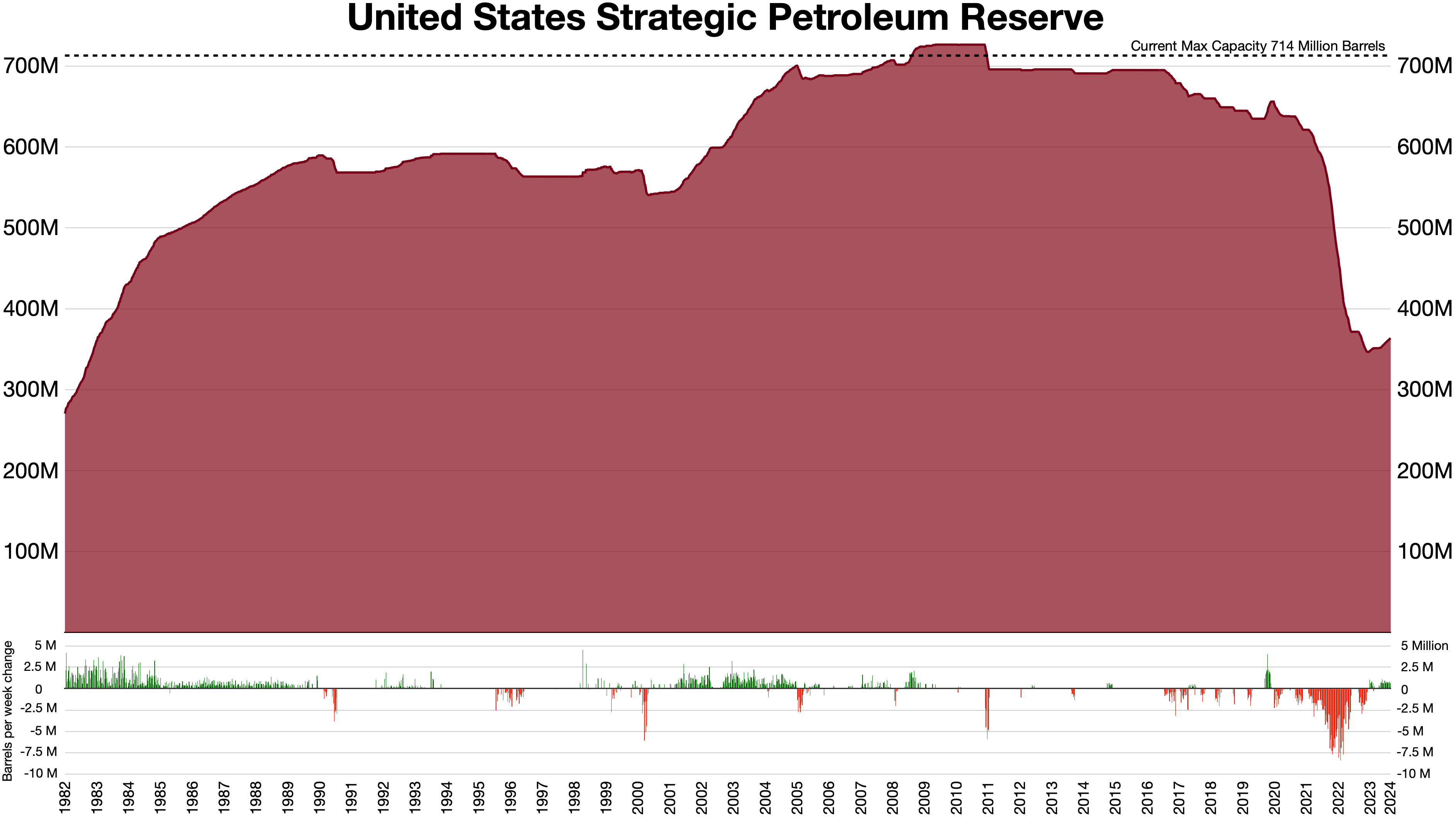

U.S. SPR Crude Falls to Lowest Since 1983, Weakening Buffer Against Oil Shocks

Severity: WARNING

Detected: 2026-06-29T17:38:11.699Z

Summary

At 17:24 UTC, new EIA data showed U.S. Strategic Petroleum Reserve crude falling by 5.5 million barrels to 325.7 million, the lowest since 1983. The drawdown leaves Washington with less emergency leverage just as Hormuz transit remains fragile and Russian fuel markets strain, increasing the impact of any future supply disruption on prices and policy.

Details

U.S. emergency oil protection has thinned to a four‑decade low. At 17:24 UTC, the Energy Information Administration reported that Strategic Petroleum Reserve (SPR) crude inventories fell by 5.5 million barrels to 325.7 million, the lowest level since 1983. The move further reduces Washington’s ability to blunt external supply shocks at a time when Middle East transit and Russian fuel supplies are already under pressure.

Confirmed details: The data, released by the U.S. EIA, show a substantial weekly draw specifically from the SPR, not just commercial stocks. At 325.7 million barrels, the reserve is now less than half of its historical peak levels above 700 million barrels. The report does not itself specify whether the draw reflects mandated sales, restocking delays, or operational moves, but it confirms the absolute volume of emergency crude available to the U.S. government has hit a multi‑decade low.

The human and industry stakes are concrete. For U.S. households and businesses, a thinner SPR means that any future price spike from a tanker incident in Hormuz, a major refinery outage, or escalation involving a key producer will transmit more directly to gasoline, diesel, and jet fuel prices. Refiners, airlines, logistics firms, and power generators lose some of the policy cushion that has historically damped price spikes. For oil producers and trading houses, a smaller SPR raises both price upside in a disruption and the volatility profile of crude curves and crack spreads.

Strategically, the U.S. government now has less physical leverage to manage crises involving major producers or chokepoints. With Hormuz traffic recently constrained by Iranian actions and Russia experiencing internal fuel supply strains, the probability of a shock that cannot be comfortably absorbed by spare capacity and inventories rises. U.S. allies that have relied on coordinated IEA stock releases also face a reduced American contribution if a multi-country release is required.

Market and economic pressure points are clear. A diminished SPR tends to be supportive for Brent and WTI, particularly the prompt months, and may widen geopolitical risk premiums embedded in options. Energy equities, especially U.S. upstream and integrated majors, stand to benefit from higher expected volatility and tighter long‑term balances. Conversely, fuel‑intensive sectors—airlines, container shipping, trucking—face higher tail‑risk for input costs. Oil‑linked currencies (CAD, NOK, some EM exporters) may gain relative to importers if traders reposition around supply‑shock scenarios.

Over the next 24–48 hours, watch how front‑month Brent and WTI react to the EIA release and whether implied volatility in crude options rises. Monitor any commentary from the White House or the Department of Energy on SPR policy—particularly signals on the timing and pace of refilling versus further releases. Also track concurrent geopolitical risk: additional friction in the Strait of Hormuz, significant disruptions in Russian exports, or new OPEC+ guidance would now punch harder into markets given this thinner U.S. emergency buffer.

MARKET IMPACT ASSESSMENT: Bullish for crude and refined products; raises geopolitical risk premium given weaker U.S. buffer against further Hormuz or Russia-related supply hits; supportive for energy equities and oil-linked currencies; potentially negative for fuel-sensitive sectors (airlines, shipping) if traders price in higher volatility.

Sources

- OSINT